The best business books reveal the method behind our most incisive decisions. They make us see the fundamental patterns that have been playing out invisibly, under our noses but beyond our notice. Often such books give us a narrative. Steve Blank showed us the plot line of a start-up, around which all else is elaboration. Clay Christensen showed us that disruptive innovation has a plot line, too, a set of implacable dynamics that play out in predictable ways from steel mills to microchips.

Leo Tilman and General Charles Jacoby’s Agility: How to Navigate the Unknown and Seize Opportunity in a World of Disruption, released today, achieves this lofty standard in a different way. Reading the book, I feel like a child who has just been given a microscope. Where my naked eyes strained to see beyond a blur, there’s structure and pattern, I can suddenly see the mechanics of how things work. And what this microscope enables us to see is one of the things that matters most in any enterprise: how it adapts as the world shifts.

The book works out the implications of a single sentence, which defines agility:

The organizational capacity to effectively detect, assess and respond to environmental changes in ways that are purposeful, decisive and grounded in the will to win.

Looking back on a career that’s moved forward largely by my attempts to grow into the spaces opened by my clients’ wisest questions, this sentence sharpened my understanding of one of my most formative experiences as an advisor. Early in 2008, Bob Selander, then CEO of MasterCard, framed an unusual brief. MasterCard’s strategy was working beautifully. The company was doubling down. And, at the same time, he recognized that the world could change in ways that would cause the strategy to be insufficient or wrong. Those changes might be abrupt. They might be gradual but engulfing, like a rising tide. Without compromising his team’s focus on execution, he needed MasterCard to develop a discipline of looking outwards, and a discipline to be intentional about how to relate to a range of scenarios for how the future might unfold.

This work taught me profoundly.

In the summer before the collapse of Lehman Brothers, leaders and directors at MasterCard were working through a scenario called “Downward Spiral.” This scenario began with a financial crisis and a major global recession, which ushered in dramatically expanded regulation. This scenario differed from what actually unfolded in one big way. In MasterCard’s scenario, interchange fees (the payment processing fees that card networks charge merchants) were aggressively targeted in the regulatory wave – whereas, in how events actually played out, the payments space wasn’t a significant focus. The concern for the financial health of the banking system worked against any changes to interchange fees, preventing real disruption of the profit pools in card payments. MasterCard thought hard about a “Downward Spiral” well before the collapse of Lehman, engaging the board as well as senior management, which created readiness to be able to respond to changes in their environment that could come quickly and could dramatically change their strategic context. As in a military context, the time to run war-games isn’t the moment of deployment. MasterCard could respond intentionally and effectively to an economy in crisis, and at the same time could perceive the points of divergence from the scenario they’d prepared, adjusting their view of risks and their strategic response accordingly.

Just as significantly, this discipline of looking outwards pointed to the ways that MasterCard needed to wire its organization differently. One of the “gradual but engulfing” forces that stood out as significant was mobile payments. At that point in time, the greatest advances in mobile payments were happening in small markets, places like Kenya. In order to navigate this space and to formulate the right offense and right defense in major markets, MasterCard needed to put small markets in a strategic spotlight and to connect dots across regions. This required pulling up insights about market developments to senior executive levels, even though these insights had only a trivial impact on the company’s core business. Per William Gibson’s dictum, “the future is already here, it’s just not very evenly distributed,” the future was manifesting much earlier in Nairobi than in New York, and the company’s attention needed to shift to where the future was surfacing first.

I see now that what we were scratching our way toward Tilman and Jacoby’s sentence.

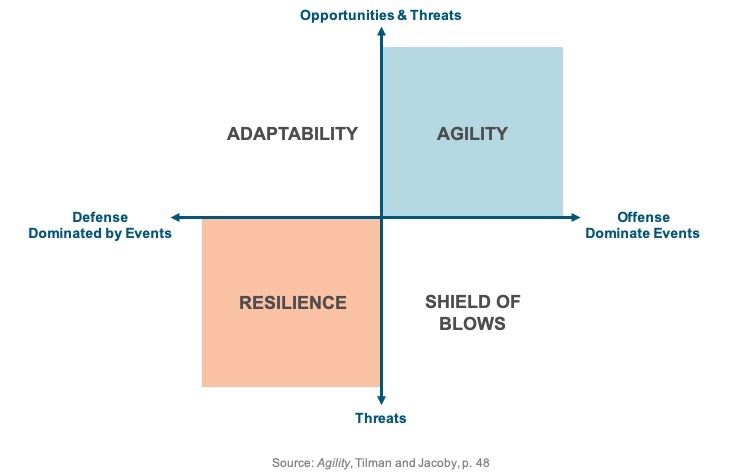

I’m embarrassed by how often I’ve fallen into the trap of seeing Enterprise Risk Management as defensive, technical, an exercise in comprehensive documentation and contingency planning rather than part of the organic fabric of strategy and innovation. Tilman and Jacoby draw a simple 2 x 2 that gives a precise diagnosis of this intellectual mistake: I was limiting consideration of risk to the lower-left imperative to achieve resilience in the face of potential harms, rather than taking a four quadrant view, which would allow focus on the offensive, dynamic potential for agility in the upper right.

Tilman and Jacoby show us the pathologies that cause organizations to fall short of agility, and paint a picture of what leadership “on the battlefield” to deliver agility looks like. They show us Bear Stearns and Wachovia steering by a certain mental model of their business, even as their actual business, and the actual nature of their risks, evolved into something very different. They contrast companies like Kodak playing assiduous defense, with companies like IMAX recognizing the need to play new forms of offense in a shifting landscape – even when the pressures of delivering a turnaround could have made it feel impractical to reach beyond their knitting.

Turning the pages, I experience a recognition of what the experience of running a business is really like: one has clear strategic ideas and compelling tactical goals, certainly, but as one moves through “fog and friction,” it is almost impossibly hard to tell if one is seeing the relevant changes in the business and in the world clearly, let alone addressing them sufficiently. To bring this to life, I’ll paint a picture of what it might have meant in my last leadership “rodeo,” as co-founder and Managing Partner of Katzenbach Partners, to have more fully exemplified Tilman and Jacoby’s formulation of agility.

Agility teaches us to look at organizations as portfolios of risks, and frames the “strategic calculus” of pursuing long-term goals as the art and discipline of matching risk to the capacity to accept risk and withstand the consequences. Looking backwards, viewing Katzenbach Partners as a portfolio of risks in the mid-2000s (e.g., in 2005 as a $40M firm with a team of approximately 100), I see us navigating five core risks of different kinds.

- Financial Risk: could we successfully match supply of advisory services with demand, and manage our cost structure to grow organically within the envelope of our financial resources?

- Senior Talent Risk: could we hold together an expanding core group of partners and principals driving the business, without losing key people and without loss of will?

- Cultural Risk: could we avoid dilution of the “special sauce” critical to creating a distinctive experience for team members and clients?

- Competitive Risk: could we sustain and sharpen differentiation even as growth caused our business model to become more and more symmetrical with much larger competitors (e.g., McKinsey, BCG)?

- Industry Risk: could we withstand, or potentially even capitalize on, the disruptive pressures operating on the industry as a whole (e.g., increased diffusion of consulting talent enabling clients to build their own capabilities or access capabilities in lower-cost models; substitution of technology and expertise delivered in other business models for consulting)?

Much of the art of building and leading the firm involved a delicate balancing act among the first three risks. Hiring ahead of demand and building a talent base from the bottom up through campus recruitment positioned us to manage cultural risk well, even as we grew 25 – 30% per year over a period of several years – but at the cost of amplifying financial risk. So long as we could achieve our target of 30% operating margins before bonuses and profit sharing, we could deliver competitive senior compensation even as the partners self-financed the firm’s growth and the development of the infrastructure we’d need for the long march toward building a lasting institution. Bringing in senior talent from the outside was essential in managing our growth, but then required careful management to navigate cultural risk and to ensure that we didn’t default to competing symmetrically with larger firms who could always outduel us on industry knowledge and analytical depth.

This balancing act worked well, so long as we executed our ambitious growth plans – but it also created a certain amount of fragility regarding how we’d absorb the spike of financial risk, senior talent risk and cultural risk that would inevitably follow from, at some point, failing to execute. I could certainly have benefitted from Tilman and Jacoby’s spotlight on the question of capacity. In building an institution to last, having the strength to withstand reversals is at least as important as building the execution disciplines to avoid suffering reversals in the first place. That said, the deeper learning from Agility in reflecting on my own experience lies elsewhere. When we made the decision to sell to Booz & Company in 2009, we’d already navigated through the failure to achieve our growth plan in 2007 and through the worst of the financial crisis in 2008 and early 2009. Financial risk and senior talent risk were still high, but probably not beyond the bounds of our capacity to navigate if we’d had sufficient will. My own reasons to favor the sale were, in hindsight, much more about competitive risk and industry risk: even if we could place ourselves back on a growth path, this seemed likely to make us more and more like other firms (less and less differentiated in how we competed), even as these firms were engaged in an increasingly intense battle with one another (industry risk), fighting for share of mind and share of wallet serving the world’s largest enterprises. We’d need to join this fight without the full complement of industry depth, functional breadth and geographic reach that the much larger consulting firms viewed as table stakes. As it turns out, even after we sold, Booz & Company struggled with the same mix of competitive and industry risks, and less than five years after made its own exit to PwC.

Tilman and Jacoby’s lens makes clear that part of my mistake in those years was that I didn’t synthesize competitive risk and industry risk as requiring equal attention as the trio of financial risk, senior talent risk and cultural risk that consumed the lion’s share of my attention as Managing Partner. Had I synthesized better, what might it have looked like to achieve “the organizational capacity to effectively detect, assess and respond to environmental changes in ways that are purposeful, decisive and grounded in the will to win”?

One of the material shifts in the consulting industry landscape in the last fifteen years has been the integration of design and innovation capabilities with strategy, organization, operations and technology. The seeds for this were planted well before our journey at Katzenbach began. IDEO was founded – formed in a merger – in 1991. In 2002, a few years into building Katzenbach, we already had the early makings of a design capability, with firm member HK Dunston, who had grown up in a formative period in the development of the disciplines of user interface and experience design. We built a small, excellent team around HK, and did a small amount of beautiful work. But we never did what Agility could have taught us to do:

- Assessed

the ascendancy of design and the value of integrating design with strategic consulting capabilities as important and lasting forces

- Responded

to that assessment at that strategic level

- Held ourselves to the standard of decisive responses grounded in the will to win, investing where we could materially address competitive and/or industry risk, and otherwise increasing capacity by preserving financial resources

Looking back at the period, Fahrenheit 212, a firm I later advised, was founded in 2004 with a vision of combining “money” (strategy) and “magic” (design). SYPartners, which has subsequently best combined design with the strengths on organization and culture that were at Katzenbach’s core, was founded in 1994 but experienced a point of inflection in its growth over the past decade. We were well positioned to capitalize on the same context that drove Fahrenheit’s and SYP’s success – and may well have chosen to exit, as both of those firms did, but with significantly expanded opportunities for organic growth along the way. Looking back through the lens of Agility makes apparent that with a clearer view of how risk shapes strategic calculus, we could have traded a bit more financial risk and a bit more senior talent risk (given internal controversies about whether design capabilities were worth investing in) in return for a more decisive experiment to see whether design could help us address the competitive risks that we ultimately deemed to be central.

This is simply one example, and I could play out a number of others as I reflect on our ten-year arc of building a firm. Agility sheds light on how, like many clients I’ve served, we at Katzenbach were savvy at detecting and often assessing environmental changes, often in the early innings of important trends – but we fell short on connecting this understanding to a sufficiently holistic picture of the risks we faced, in order to determine where the “will to win” required more decisive offense, and where we should have played stronger defense in order to preserve capital and capacity.

These are essential questions for every CEO and every founder. The field of enterprise risk management has too often and for too long been practiced as a litany of ways to be watchful and careful. Agility shows us that powerful, strategic thinking about risk positions us to play better offense, to seize the moment when we might otherwise settle for a small advance. Especially for those of us who have the aspiration to build or to steward an institution that can weather the years – as we did at Katzenbach, and we do with even greater conviction at Incandescent – Agility should take a place at the very core of how we think about strategy and how we build organizations that can flourish amidst the tumult of uncertain times.